Key points

- The Contracts for Difference scheme has been key to the expansion of cheap, homegrown renewables by bringing investors certainty, and lowering the cost of capital

- The cost to develop and build projects has risen significantly in recent months due to regulatory uncertainty and supply chain pressures

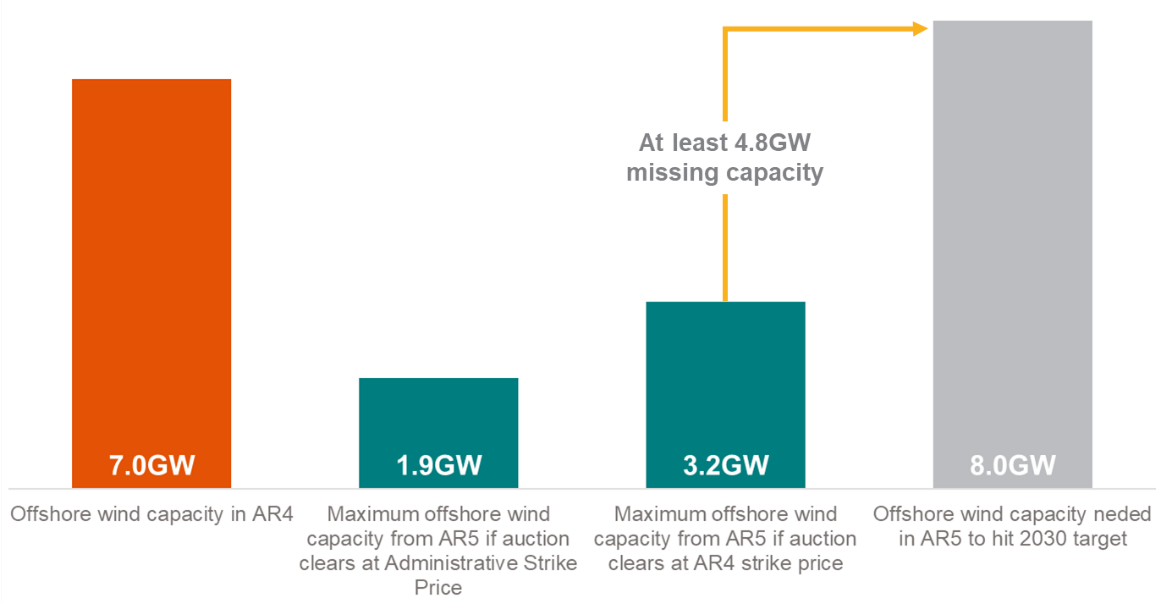

- Energy UK analysis shows that the latest renewable auction round (AR5) will fall short of at least 4.8GW of offshore wind capacity due to an insufficient budget and poor price mechanisms that have not taken current market factors into account.

- This lost capacity is enough to power nearly 5.5 million homes with clean energy, and risks costing consumers up to £530 million due to our reliance on expensive, imported gas.

- It also puts into question future investment in clean technology at risk, and jeopardises the UK’s energy security targets

The cost to deliver offshore wind has changed

- The Contracts for Difference (CfD) scheme is the cornerstone of the UK’s clean energy strategy. Since its introduction in 2014, the CfD programme has played a key role in derisking investment, bringing down the cost for renewables such as offshore wind, and cementing the UK as a global leader in this technology.

- Combined with long-term Government targets, by agreeing a stable Strike Price industry and the supporting supply chain has been able to invest in the UK with confidence, slashing costs by nearly 80% in less than a decade.1

- For mature technologies like offshore wind, the prices agreed for CfDs are low enough that their primary function is no longer to subside investment, but to provide the certainty investors need to keep costs low. This means that CfDs are currently paying back to consumers; the latest price cap is £54 a year lower from CfDs2.

- A combination of inflation, interest rate increases pushing up financing costs, a supply chain crunch, and regulatory uncertainty through systemic problems with grid connections and planning have led to higher overall project costs in recent months.

- CfD auctions are now held annually. This positive development requires re-evaluating financial and supply chains conditions on a more regular basis.

- There are significant concerns that the latest CfD round, Allocation Round 5 (AR5) does not recognise the scale of cost increases seen over recent months.

The role of CfDs in achieving energy security and a decarbonised power sector

- The Government aims to decarbonise the power sector by 2035, and within this context has set a target for the UK to have 50GW of offshore wind by 2030.

- In the context of declining North Sea hydrocarbon production and forecast rising demand for electricity, ensuring domestic sources of clean energy is even more important.

- The Climate Change Committee shows that in every scenario, large scale offshore wind is needed to meet our Net Zero targets

- CfD’s remain the only realistic option to deliver large scale offshore wind3.

Around 27GW of offshore wind capacity is either already in operation or has been awarded a CfD and is set to be delivered by 2030. That means an additional 23GW must be delivered through upcoming Allocation Rounds.

Delivered and forecast offshore wind capacity needed to reach 2030 50GW target

Source: Energy UK analysis of LCCC CfD register and Ofgem ROC register

Given substantial lead times to develop and build projects, we assume this will be split evenly between three Allocation Rounds (AR5, AR6, AR7), meaning each allocation round will need to deliver around 8GW of offshore wind, more than any historically.

Likely outcomes from AR5 auction

- Offshore wind sits in AR5 auction Pot 1, with solar and onshore wind.

- The capacity delivered by AR5 will be determined by the bids which developers place in the auction. This is limited by a combination of the auction budget, and the difference between the guaranteed price of electricity set by the auction (the Strike Price) and a Reference Price.

Given supply chain pressures and the rising cost of capital, it is unlikely that the Strike Price of offshore wind will be any lower in AR5 than it was in AR4, and it is subject to a ceiling in the form of the Administrative Strike Price.

Using the range of possible AR5 strike prices based on the difference between AR4 Strike Prices and the AR5 Administrative Strike Price (£37.35/MWh-£44.00/MWh), and assuming 100% of the budget is allocated to offshore wind, a maximum of 3.2GW could be secured in the next auction.

The resulting offshore wind capacity will be less (probably significantly), due to onshore wind and solar projects sharing the same overall funding4.

Source: Energy UK analysis

The consequences of missing capacity

- With 8GW of offshore wind required in AR5 and an estimated maximum of around 3.2GW expected to come through, the amount of offshore wind capacity delivered by AR5 will almost certainly be at least 4.8GW short of what is required to meet the 2030 target, and the gap is likely to much greater.

- Even 4.8GW of lost capacity is a significant shortfall. The power that would have been produced by those windfarms will instead have to be generated using gas, most of which is likely to be imported. This has serious consequences for consumers, the economy, and the environment;

- Capacity that could power 5.5 million homes every year

- £530 million every year in extra costs to consumers by 2030.

- 6 m tonnes of carbon emissions per year from unabated gas generation.

- Even more capacity will be needed in future auction rounds, amidst growing international competition for vessels, supply chain and skilled workers

- Missing a vital window for investment by sending the wrong signals to global developers and manufacturers; once projects and factories are located outside of the UK, future projects will be harder to secure at lowest costs.

- Putting the UK at risk of losing its position as a global leader in wind power and missing the opportunity to become a world leader in growth technologies such as floating offshore wind.

Why is AR5 unlikely to deliver?

- The overall budget for AR5 is £80m less than AR4, and as shown above, is simply not large enough to bring forward renewable capacity consistent with the Government’s own targets.

- The change in pot structures down from three in AR4 to two in AR5 means offshore wind is now competing with other established technologies, for less funding.

- The Administrative Strike Price (ASP), i.e. the auction price ceiling, does not go far enough in recognising the scale of cost increases experienced by developers over recent months. A low budget combined with a low ASP is likely to result in fewer projects, all priced at or close to the ASP level, eating up all of the budget but delivering less capacity.

- The Reference Prices (projected electricity market prices) used in AR5, which underpin the investment case for developers, are unrealistically low and inconsistent with the vast majority of publicly available wholesale electricity price forecasts.

Future wholesale electricity prices

Source: Energy UK analysis of DEZNES and OBR

What actions could Government take to reduce the shortfall, ensure we meet our net zero and energy security targets?

- Revisit and increase the AR5 budget

- Raise the Administrative Strike Price to recognise the increased costs to develop and build critical infrastructure projects in the current climate

- Produce a robust response to increased global competition for clean energy from the US and EU (such as the Inflation Reduction Act) in the upcoming Autumn Budget.

1 From up to £209.32/MWh in the Investment Contract round of CfDs from 2014 to £45.37 in AR4 in 2022 (LCCC, 2023£s)

2 Ofgem

3 This is not the case for solar or onshore wind. Unsubsidised routes to market such as Power Purchase Agreements (PPAs) and merchant (investment without subsidy) are available for solar and onshore wind, but not as the main route to market for offshore wind with its very high upfront cost and long payback period.

4 There is an additional pot for emerging technologies such as Floating Offshore Wind and Tidal, but it is designed to deliver much smaller capacities.

Downloads

-

Energy UK AR5 response v2

Type: PDF (340 KB)