Key points

- From 1 January 2026, the European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM) will become fully active. From this date, products exported into the EU will pay a new levy consistent with the EU’s domestic carbon price: the EU Emissions Trading System (ETS).

- The implications of the EU CBAM on Northern Ireland are likely to be disruptive, expensive, and highly controversial.

- The EU CBAM will apply on certain goods crossing from Great Britain (GB) to Northern Ireland, and those produced in Northern Ireland but exported into the Republic of Ireland or other EU countries.

- Energy UK analysis shows that the EU CBAM could lead to payments of up to £200 million annually – equivalent to £1bn over the course of a Parliament – on trade between GB and Northern Ireland. This charge will be paid to the EU and increase costs for Northern Irish consumers.

- The EU CBAM will also lead to higher energy bills in the Single Electricity Market (SEM) by up to £130 million per year – equivalent to £45 per household in Northern Ireland.

- More than 1,100 Northern Irish jobs are vulnerable to the EU CBAM, more jobs than were secured in the recent purchase of the Harland & Wolff shipyard.

- If the UK Government was to block the EU CBAM being applied, there is a risk of destabilising the UK-EU relationship, damaging the SEM on the island of Ireland, and retaliatory tariffs from the EU on UK goods.

- The solution to this problem is through linking the UK and EU ETSs, which would negate the need for a CBAM between the UK and EU. There is strong industry and civil society consensus for linkage.

- The UK Government should announce its intention to initiate ETS linking negotiations at the upcoming EU-UK Summit, with the aim of concluding negotiations by the end of 2025. This will avoid the damage to Northern Ireland’s economy, and higher prices for Northern Irish consumers.

What is a Carbon Border Adjustment Mechanism?

- A Carbon Border Adjustment Mechanism (CBAM) is a policy tool aimed at maintaining the competitiveness of domestic production and preventing carbon leakage – where efforts to reduce greenhouse gas emissions in one country cause an increase in emissions elsewhere.

- A CBAM works by ensuring that imported goods pay an equivalent carbon price to what would be paid had that product been produced domestically.

- The EU’s CBAM is due to be fully financially implemented in 2026 and is currently in a two-year trial implementation phase. The UK is introducing its own CBAM in 2027. They are largely similar in scope, covering carbon-intense products such as steel and cement. However, unlike the UK CBAM, the EU CBAM will include electricity.

- Following the UK’s departure from the EU, the UK implemented a separate emission trading scheme (ETS). Despite initially tracking the EU ETS price closely, UK ETS prices have collapsed over the last 18 months. The UK currently prices carbon lower than in the EU[1] although future carbon prices are uncertain and could change.

- The lower UK carbon price means that businesses exporting from the UK into the EU will need to pay up to £800m annually in CBAM charges with an additional administrative burden that creates further barriers to trade.[2]

Where does Northern Ireland come into the picture?

There is uncertainty about where and how a carbon border would be applied. In the most likely scenario, the following will be established:

A carbon border between GB and Northern Ireland

- The EU is likely to insist that its CBAM applies in Northern Ireland. The CBAM would apply both east-west (to goods crossing from GB[3] to Northern Ireland) and north-south (to goods produced in Northern Ireland but exported into the Republic of Ireland).

- Only by applying the CBAM in both the Irish Sea and on the border between Northern Ireland and Republic of Ireland will the EU be able to confirm that any goods entering the European single market have paid a carbon price equivalent to the EU ETS.

- In practice, this means that huge swathes of goods moving from GB to Northern Ireland and from Northern Ireland to Republic of Ireland would have to fill in complex paperwork detailing carbon intensity and would likely face a substantial new levy.

- In the case of GB to Northern Ireland trade, it is particularly problematic that goods moved within the UK would face a tax which is collected by the EU.

- For this to take effect, the EU would have to take action under Article 13(4) of the Windsor Framework, as set out by the Sunak Government.[4] The EU would need to request that its CBAM apply in Northern Ireland, which would be subject to approval from the UK Government and followed by a vote in the Stormont Assembly. To date, no such action under Article 13(4) has been taken.

- The position of the Sunak Government was that the EU CBAM should not apply to Northern Ireland, but the current Government has yet to publicly confirm its approach.

- If the UK was to insist that the EU CBAM should not apply in Northern Ireland, this would have serious consequences for the Government’s ‘reset’ with the EU and risk reopening the Windsor Framework. A likely consequence of this action would be the imposition of barriers to trade in the form of retaliatory tariffs from the EU.

A carbon border for electricity between GB and the Irish SEM

- Electricity generators in Northern Ireland are covered by the EU ETS as part of the provisions that create the SEM on the island of Ireland.

- With the EU CBAM in place, any electricity exported from GB to the Republic of Ireland will have to pay an additional fee based on the relative carbon price differential between the UK and EU. If the EU requests the addition of the EU CBAM under Article 13(4) of the Windsor Framework – as it is likely to – this charge would also apply to electricity exported to NI.

- There are concerns about how a CBAM would be applied to electricity. It is highly likely that exported electricity from GB would need to use a default emissions value based on outdated data about the marginal carbon intensity of the grid.

- The EU CBAM has not set out how a carbon price paid in the UK would be accounted for. This could mean both that wind and solar power dispatched from GB to Northern Ireland/Republic of Ireland will subject to a CBAM charge, and that GB gas generation sent to Northern Ireland/Republic of Ireland will pay an additional carbon price that it will already have paid through the UK ETS.

- Furthermore, high exports of electricity from GB will be at times of high renewable generation – meaning it will have a far lower carbon intensity than the system average. The EU CBAM risks deterring investment in clean homegrown energy in any market connected to GB and raising bills across the UK and EU with limited environmental benefit.[5]

What are the implications of this?

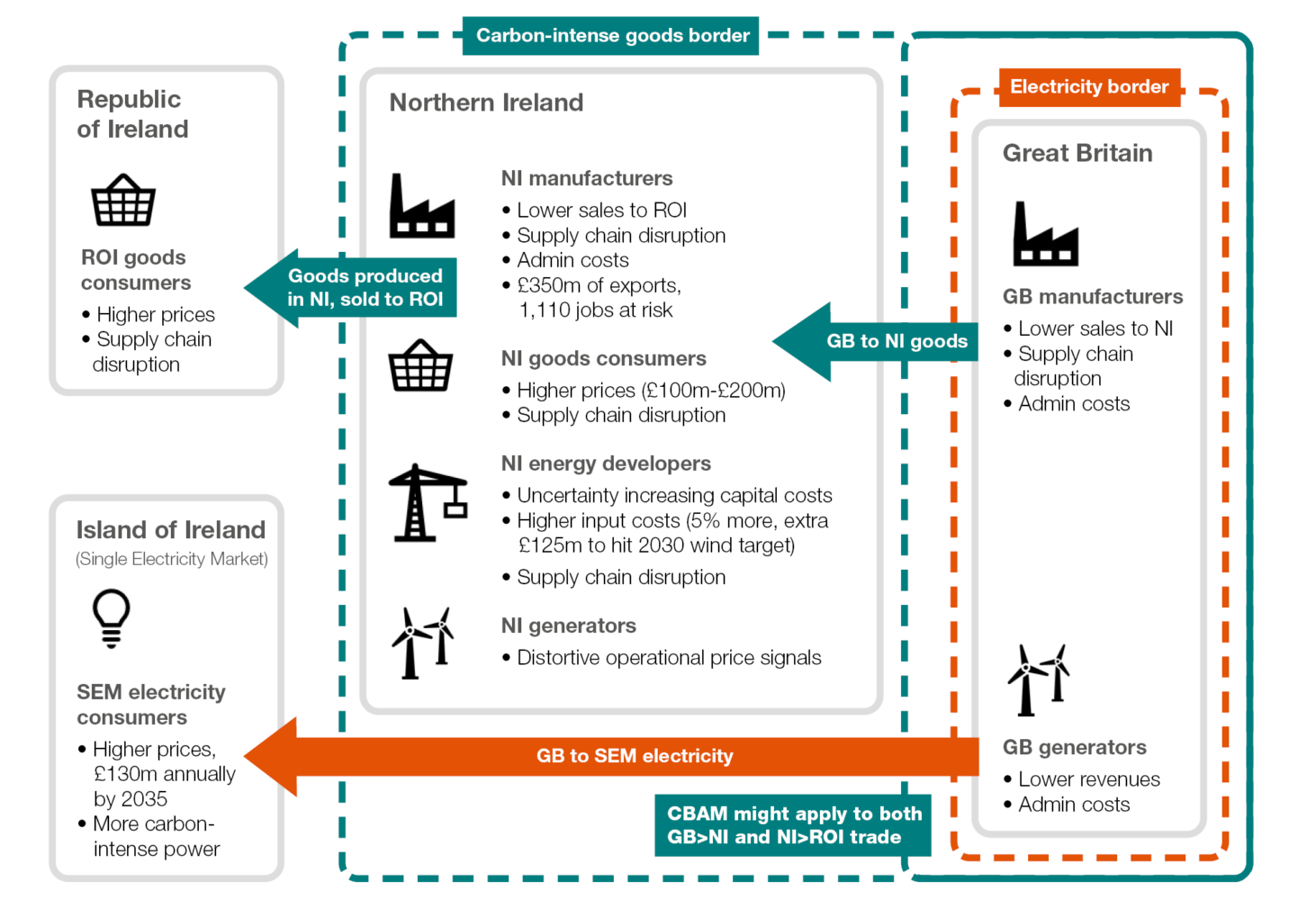

Figure 1: Potential consequences of the application of a CBAM in GB and the island of Ireland

Costs on goods and disrupted supply chains

- Exports worth £350m and more than 1,100 jobs are vulnerable to the EU CBAM in Northern Ireland.[6] That is more jobs than were secured in the recent purchase of the Harland & Wolff shipyard.[7]

- The EU CBAM will have both cost and administrative implications for trade between the UK and EU – even if carbon prices are aligned.

- There is significant uncertainty about how EU CBAM liabilities would be calculated, particularly for sectors with complex, international supply chains. For example, it is unclear how a CBAM liability be calculated if an EU-produced component used in the construction of offshore wind uses steel from outside of the EU, is then shipped to the UK for assembly, installed in Irish waters and serviced from a GB port.

- We estimate that there could be CBAM payments of between £100m-£200m annually – or up to £1bn over the course of a parliament – on trade between GB and Northern Ireland.[8]

- If the UK CBAM, rather than the EU CBAM, applied in Northern Ireland, there could end up being a red/green lane system for CBAM goods based on whether it was intended for the EU internal market – similar to the system for goods under the Windsor Framework. However, this would require reopening the Windsor Framework process and place a significant administrative burden on businesses wanting to trade between GB and Northern Ireland, disrupting supply chains and clean investment in the region.

Uncertainty

- The EU CBAM has already proved challenging to implement during its 2024-25 phase-in period.

- While industry can reasonably assume that a carbon price paid in GB will be recognised by the EU, this will not be confirmed by the European Commission until the final three months of 2025 – with the first payments under the EU CBAM regime being applied from 1 January 2026.[9]

- Electricity is mostly traded significantly ahead of time. Uncertainty about how, or even if, an EU CBAM would apply to electricity trade between GB and Northern Ireland impacts current trading in the SEM. This uncertainty means that suppliers may under-hedge or over-price a CBAM charge, both of which have the net impact of raising electricity costs for customers.

More expensive, higher-carbon electricity

- The EU CBAM will apply to electricity imported into the EU. To preserve the integrity of the SEM, the EU may expect that the EU CBAM to apply on electricity imported into Northern Ireland.

- The EU CBAM methodology will penalise clean electricity generation from GB. Inefficient trading, including overcharging for imports at times of high renewables output in GB, could raise wholesale electricity prices in Ireland and Northern Ireland, potentially ramping up to £130m in annual costs in the 2030s.[10] This means that electricity bills in Northern Ireland could be increased by the equivalent of up to £45 per household per year, due solely to an avoidable cost.

- To keep the lights on, supply and demand for electricity must match exactly in real time. The most efficient way to balance supply and demand is for the electricity price to reflect the marginal plant cost, i.e. the cost of the last, most expensive plant needed to meet demand.

- Should the CBAM make interconnection the marginal plant in the SEM then there will be considerable uncertainty about future prices for electricity in all scenarios, given it will be dependent on weekly changes in CBAM price. This exposes energy companies to significant trading risk. Any risk will ultimately be passed on to consumers in the form of higher bills.

Making it harder to reach Net Zero

- Applying the EU CBAM in Northern Ireland will have a direct impact on the cost required of meeting the UK and EU’s shared decarbonisation ambitions.

- Energy UK analysis finds that an EU CBAM could increase the cost of building a wind turbine in Northern Ireland by 5% if components/materials shipped from GB are subject to the EU CBAM – increasing the cost of delivering Northern Ireland’s expected 2030 renewable energy capacity by up to £125m.[11]

- In addition, the uncertainty and distortion of the electricity traded in the SEM is likely to increase the cost of capital for new projects and potentially make investment cases for developers weaker.

What is the solution?

- Linking the EU and UK carbon markets would remove carbon borders between both jurisdictions. ETS linkage should be a top priority for the UK Government and European Commission to provide certainty for investment and protect consumers in Northern Ireland.

- The UK-EU Trade and Cooperation Agreement requires both UK and EU to give ‘serious consideration’ to linking carbon markets.

- The EU has previously linked its carbon market to Switzerland. The similarity of both carbon markets and matching levels of decarbonisation ambition mean that linkage negotiations should be able to proceed at pace, particularly compared to previous EU linkage negotiations.

- Most importantly, by creating a combined carbon market, the carbon price in the UK and EU will end up becoming the same. This removes the need for CBAM payments from the UK to EU. With a linked carbon market, the administrative burden of filling in CBAM paperwork will also disappear.

- A linked UK-EU carbon market would go a long way to showing the UK Government is resetting its relationship with the European Union. It is also supported across the economy in the UK and Europe.[12]

We urge the UK Government and the European Union to initiate negotiations to link their respective emissions trading schemes at the upcoming UK-EU Summit. This will avoid creating further uncertainty for consumers and businesses on the island of Ireland and demonstrate global climate leadership.

For more information contact Adam Berman, Director of Policy

[1] The carbon price paid on electricity generation in Great Britain is the UK ETS price plus Carbon Price Support – a flat surcharge currently set at £18 and only paid by electricity generators.

[2] Frontier Economics (2024) Linking UK and EU Carbon Markets.

[3] i.e. England, Wales and Scotland

[4] UK Government (2024) Safeguarding the Union.

[5] Afry (2024) EU CBAM Impact Study.

[6] Zhao, X and Zhang, D (2023) Where Technical Meets Political: The Complexity of the EU CBAM in Northern Ireland.

[7] Department of Business and Trade (2024), Deal agreed to secure Harland & Wolff’s future protecting thousands of UK shipbuilding jobs

[8] Energy UK analysis of SIC code data covering Supply and Use in Northern Ireland and UK-level carbon intensity of non-electricity products that will be covered by CBAM. Where the lowest-level SIC code covers both CBAM and non-CBAM products, we have made assumptions about the share of the SIC code related to CBAM products using GB-wide low-level employment data.

[9] European Commission (2024) CBAM Informal Expert Group.

[10] Afry (2024) EU CBAM Impact Study.

[11] Energy UK analysis, with 2030 capacities based on “Self-sustaining 2030” scenario from SONI (2024) Tomorrow’s Energy Scenarios.

[12] UK and EU Trade and Cooperation Agreement Domestic Advisory Groups (2024) Joint Statement.

Downloads

-

Energy UK Explains – Carbon Border Adjustment Mechanisms in Northern Ireland

Type: PDF (434 KB)