The events of the past few weeks have been a stark reminder of just how fragile the global energy landscape remains and how exposed the UK economy is to developments far beyond its borders. Renewed geopolitical tensions, volatile gas markets, and persistent concerns over industrial competitiveness reinforce a simple truth: in an increasingly uncertain world, international cooperation in critical sectors like energy is more important than ever. For the UK and the EU, which share a deeply interconnected energy system, rebuilding cooperation is essential to resilience.

That is the context in which the UK-EU reset should be understood. Across emissions trading, electricity market integration and the commitments emerging from the Hamburg Summit in January, there is a clear opportunity to strengthen the resilience of Europe’s energy system and protect households, businesses, and the wider economy from future shocks.

Linking the UK and EU Emissions Trading Schemes (ETS) stands out as one of the most immediate opportunities. The two systems are fundamentally similar, with the UK ETS closely modelled on the EU’s and both evolving in similar directions, expanding to sectors such as shipping and exploring the role of greenhouse gas removals.

Yet carbon pricing has come under increasing political pressure on both sides of the Channel in recent months. Concerns over industrial competitiveness and consumer costs have led some to question whether emissions trading can endure in its current form. But scrapping or suspending carbon pricing would be a strategic mistake. Pricing emissions sends a clear signal to invest in cleaner, locally generated energy that is less exposed to global fossil fuel volatility. The ETS remains one of the most cost-effective tools for delivering this, by incentivising emissions reductions to occur where they are cheapest first. In a world of constrained public finances and intense global competition for clean investment, that efficiency is indispensable.

There is also the crucial question as to how ETS revenues are used. Unlike the UK, the EU has made it mandatory for member states to spend 100% of EU ETS proceeds to finance decarbonisation projects. For the most part, member states follow this rule, albeit with some exceptions. At a minimum, the EU does at least have a structure to ensure some revenues are spent on electrification and reducing dependence on fossil fuels; the UK could learn lessons from this.

Investors are not calling for carbon pricing to be weakened, but for it to be more stable, predictable and clearly linked to supporting the transition.

Linkage positions the UK alongside the EU as a rule-shaper in an emerging low-carbon trading system, rather than a rule-taker.

Linkage would address several of these challenges. A larger, more liquid carbon market is inherently more stable and less prone to volatility, strengthening investor confidence. It would also reduce trade frictions. Without linkage, UK exporters could face carbon costs under the EU’s Carbon Border Adjustment Mechanism (CBAM), with estimates suggesting this could reach £800 million annually by the end of the decade. More broadly, as carbon pricing spreads globally, linkage positions the UK alongside the EU as a rule-shaper in an emerging low-carbon trading system, rather than a rule-taker.

A similar logic applies to electricity market coupling. Before Brexit, the UK participated in the EU’s internal energy market, using coordinated “day-ahead” trading to optimise cross-border electricity flows. Since then, inefficiencies have added an estimated £120-£370 million annually to system costs, and ultimately consumer bills. Reintroducing more efficient trading arrangements would therefore deliver immediate economic benefits.

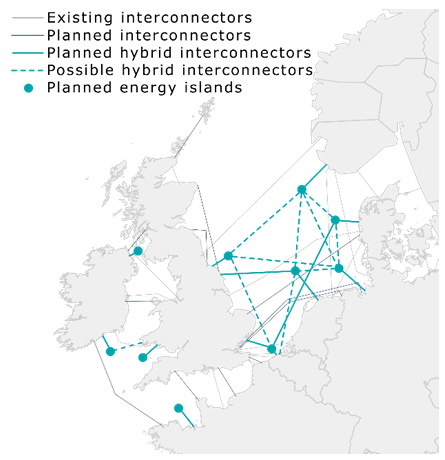

But the deeper value lies in resilience. As energy systems become more decentralised and reliant on variable renewables, flexibility becomes the cornerstone of energy security. Interconnectors linking Britain with neighbouring markets allow countries to share surplus power, balance intermittency, and respond to shocks. The UK is on course to reach 12-14GW of interconnector capacity with Europe by 2030, making it one of the largest sources of system flexibility not tied to volatile global gas markets. More effective market coupling ensures these assets are used efficiently, reducing costs while strengthening security of supply.

Without aligned trading arrangements, electricity cannot flow efficiently to where it is most needed, undermining investment confidence in this crucial resilience measure.

Looking ahead, offshore “hybrid” projects in the North Sea will take this further. By combining wind generation with interconnection, these assets create a more integrated, flexible system, effectively using the North Sea as a shared, webbed “battery”. However, much of the success of this infrastructure depends on closer market integration. Without aligned trading arrangements, electricity cannot flow efficiently to where it is most needed, undermining investment confidence in this crucial resilience measure.

Figure 1: Existing and planned interconnectors and Hybrid Interconnectors in the North Seas

Sources: ENTSO-E ONDP, ENTSO-E TYNDP 2022 and ENTSO-E, taken from grid map by Elia

The Hamburg Summit in January 2026 marked a step change in this approach, signalling a shared political commitment across the North Sea to deeper cooperation. ETS linkage and improved electricity trading are only the first steps. The declaration highlights joint work on offshore wind deployment, targeting 300GW by 2050, coordination of planning and permitting, joint supply chain development and stronger protection of critical energy infrastructure. Taken together, these measures reflect a recognition that energy security in between the UK and EU is indivisible.

That said, closer cooperation inevitably involves trade-offs. Greater alignment may be required in areas such as emissions trading rules, state aid frameworks, and aspects of energy regulation across energy wholesale, retail, renewables support and permitting policy. These are legitimate considerations, and they will be central to UK-EU negotiations in the months ahead.

However, the direction of travel is clear. The costs of fragmentation, higher prices, reduced investment certainty and weaker resilience, are increasingly difficult to justify. By contrast, cooperation offers lower costs, stronger security of supply and a more investable clean energy system. Plans for a joint governance framework on energy and climate policy could, for the first time since Brexit, put the UK back “in the room,” helping to shape the rules that will define Europe’s energy future.

Tobias Burke is Policy Manager for UK–EU energy and climate relations at Energy UK. He leads work on cross-border energy policy, including emissions trading, interconnection, market integration, and regulatory alignment, to support the UK and EU’s transition to a more secure, competitive and low-carbon energy system.