Upgrading millions of homes this Parliament relies on unlocking the power of the private sector. This paper explores the policies that are needed to attract capital investment from both households and investors into the clean heat transition.

Energy UK analysis shows that investing £1.5 billion of the Warm Homes Plan budget into subsidising green home finance would unlock up to £9 billion of additional consumer investment, supporting up to 950,000 middle-income households to access low-carbon technologies.

For an accessible version of this report, please email press@energy-uk.org.uk.

About this series

This is the second of Energy UK’s Clean Heat series of policy reports, which aim to explores the actions needed to attract capital investment from both households and investors into the clean heat transition.

The first report, Clean Heat: Balancing the bill, analyses the cost to HM Treasury of rebalancing policy costs on energy bills alongside its economic and social benefits. Future Clean Heat reports will explore the themes of regulation, jobs and skills, and consumer engagement and protections.

To discuss this series – or any of our analysis – in more detail, please email press@energy-uk.org.uk or louise.shooter@energy-uk.org.uk.

Clean Heat: Financing the transition

August 2025

Executive summary

The UK Government has confirmed the £13.2 billion budget for its Warm Homes Plan following the Spending Review 2025.[1] This is a significant investment into improving the quality and efficiency of existing homes and buildings in the UK, creating a real opportunity to improve the living conditions of millions of people over this Parliament. This is critical in the context of stretched household finances and the now common belief among Britons that the cost-of-living crisis will never end.[2],[3]

In this series of reports, Energy UK shows how the transition to clean heat can be delivered in a way that lowers bills for energy customers, boosts economic growth, and creates jobs across the country. This report explores the role of finance in catalysing the capital investment needed to switch from fossil fuel to clean heating systems such as heat pumps, heat batteries, and low-carbon heat networks. The tens of billions of pounds of investment is also contingent on reducing electricity costs, which was explored in the first paper in this series.[4]

Nearly three-fifths of Boiler Upgrade Scheme (BUS) customers are high-income households.[5] Energy UK analysis shows that investing £1.5 billion of the Warm Homes Plan budget into subsidising green home finance would unlock up to £9 billion of additional consumer investment into the clean heat transition. This would enable up to 950,000 households to access clean heating measures and other low-carbon technologies who would otherwise not have the funds to do so.[6]

Achieving a successful Warm Homes Plan that represents best value for money relies on our ability to harness the power of the private sector. This requires the prioritisation of policies that crowd in additional capital investment, decreasing the need for government grants in the long term. Alongside the rebalancing of policy costs on energy bills, government investment in a green finance subsidy would create a significant multiplier effect and help to reach more households for every £1 invested, compared to the impact of grant support alone for clean heat.

Combining the BUS with a low-cost loan will help households to take up clean heat at a much lower cost to government than fully subsidising the technology for middle-income households. A survey by MCS (Microgeneration Certification Scheme Service Company Limited) found that 65% of people could be encouraged to use financing options to make energy efficiency improvements, if they had access to a government grant to fund part, or all, of the measures.[7]

Capital investment is also needed to significantly increase the development of heat networks, which have the potential to deliver up to 20% of heat for buildings by 2050. The sector aims to invest £80 billion by 2050; however, barriers to investment are driving up the cost of development capital, and ultimately the cost to consumers.[8]

To achieve this most efficiently, the Government should provide support for the Green Heat Network Fund (GHNF) under the Warm Homes Plan and allocate a budget of £485 million to 2028.[9] The National Wealth Fund (NWF) also has a role to play in reducing the cost of development. It should guarantee a package of commercial development loans for projects that have successfully acquired funding through the GHNF, and work with combined authorities with regional energy strategies to deliver area-based retrofit, including heat network developments.

With the right policies in place, the Warm Homes Plan can unlock considerable private capital investment, which is key to delivering the clean heat transition.

Content

The Warm Homes Plan should subsidise green finance to help households cut bills.

How middle-income households can benefit from Government-subsidised green finance.

Bringing down the cost of finance for heat network infrastructure.

The Warm Homes Plan should subsidise green finance to help households cut bills

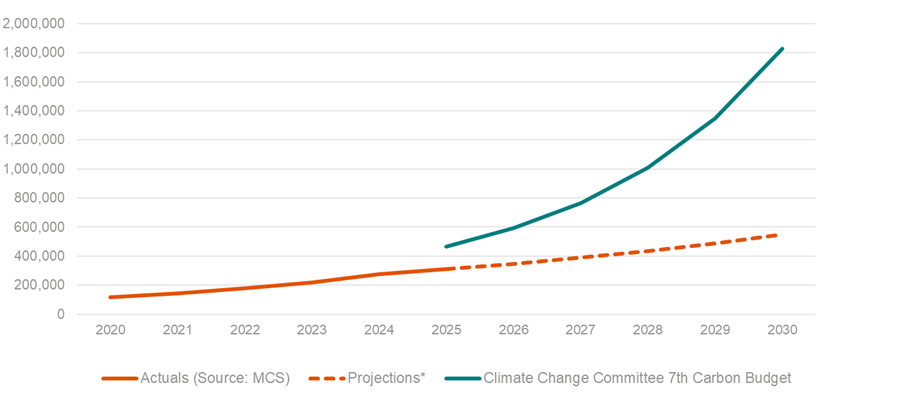

Clean heat installations need to increase dramatically in the years ahead to meet the trajectory set out under the Climate Change Committee (CCC)’s Balanced Pathway, as shown by Figure 1 (below). The rate has already risen substantially from 15,273 heat pumps in 2020 to almost 70,000 in 2024.[10] However, this needs to grow to 450,000 annual installations by 2030, and 1.5 million by 2035 for the Government to meet its targets.[11] Three per cent of homes are currently heated by a heat network, all of which will eventually be decarbonised under forthcoming regulation.[12] This market share needs to increase to 9% by 2040 for the UK to keep on track with its decarbonisation targets.[13]

Figure 1: Cumulative heat pump installations from 2020 to 2030, actuals with projections and expected by CCC.[14]

A key barrier to growth in the clean heat sector is the running costs, compared to gas. As explored in Energy UK’s ‘Clean Heat: Balancing the bill’ and ‘Reducing non-domestic electricity prices to drive economic growth’ papers, the cost of electricity for both households and business customers is disproportionately high, due to the distribution of policy costs weighted onto the electricity bill.[15],[16] This distribution artificially inflates the cost of operating low-carbon technologies, such as heat pumps, heat batteries and heat networks. Action is needed to balance the bill and ensure clean heat is the cheapest form of heat in all scenarios. This is crucial to drive the clean transition, while it will also support economic growth and help lower prices of other goods and services for consumers.

The upfront capital cost of the technology is another key blocker to growth in the clean heat market across all technology types. The CCC estimates that £20.5 billion capital investment in low-carbon heating is needed by 2030 to reach the Balanced Pathway targets. While the £13.2 billion Warm Homes Plan allocation will contribute materially, the full investment required in the clean heat transition cannot be met by public spending, nor levied on energy bills, alone.

The typical cost for a residential building to switch from a fossil heating system to clean heat technologies, such as an air source heat pump, ground source heat pump, or connecting to a heat network, is above £10,000.[17],[18] By contrast, a replacement gas boiler typically costs between £2,000 and £3,000. Non-domestic customers will face even higher price differentials when looking to switch to a low-carbon alternative.

Many low-income households are supported by the Energy Company Obligation (ECO) and Warm Homes: Social Fund, which provide fully funded energy efficiency measures.[19],[20] However, these schemes have primarily funded the installation of fabric measures to date, such as loft, cavity and solid wall insulation. More focus on clean heat in future iterations would help to ensure low-income households benefit from efficient, flexible heating systems, mitigating the impact from any future spikes in international gas prices.

People can take advantage of the Boiler Upgrade Scheme (BUS), which provides grants of up to £7,500 toward the installation of clean heating systems and which is open to applications from all households and businesses using domestic-size systems. Households that benefit must have the necessary capital to pay the additional cost of installation, with the average air source heat pump project installed under the BUS costing £12,795 in total.[21] Most property owners that have used the BUS so far have used their savings or regular income to pay the cost not covered by the grant.[22]

Households that are neither eligible for fuel poverty schemes nor have the available savings to pay the non-grant costs, are at risk of being left behind in the clean heat transition. The Warm Homes Plan presents an opportunity for the Government to support these middle-income households by delivering on its manifesto pledge of working with the private sector to develop the green finance market.[23]

There is already reasonable availability of green home finance products in the UK, with all the largest lenders offering some form of loans that incentivise more energy efficient housing. The most common product is a green mortgage, which offers lower interest rates, increased borrowing or cashback to houses with Energy Performance Certificate (EPC) A or B ratings. Many lenders also provide cashback or low-interest products for mortgage holders to undertake energy efficiency improvements (e.g. green additional borrowing).

Moreover, energy companies are collaborating with lenders to enable low-carbon technology installations, including:

- British Gas helps its customers spread the cost of a heat pump with a £0 deposit. Financing options include 0% interest for two years, and up to 10 years with interest.[24]

- Hive offers a solar panel subscription for £0 upfront with Sunsave Plus. The subscription starts from £69/month, with a 20-year Sunsave Guarantee.[25]

- Octopus Energy helps its customers spread the cost of solar panels, through fixed-term, interest-free loans over one, two or three years, or up to 10 with interest provided by DivideBuy.[26]

- Octopus Energy has also partnered with Lloyds Banking Group to support its Green Living Reward, allowing customers to combine a heat pump installation with a £2,000 lender cashback offer and a £100 Octopus bill credit. This layering of incentives has the potential to boost the appeal of retrofit and bring down costs.[27]

- Kensa Utilities offers Ground Array Funding, which covers the cost of the groundwork for ground source heat pumps. Through this scheme, an investor funds the network, which can then charge connection fees to connected properties, which are paid over multiple years. This helps spread out the upfront cost for the property.[28]

However, the uptake of green home loans, including green additional borrowing and unsecured green finance solutions, is currently very low. There are several factors behind this:

- The savings from clean heat investments are insufficient, and many consumers have little understanding of retrofit or green home finance. Almost two-fifths of people believe that energy efficiency improvements would cost more than the amount they would save over the lifetime of the measures.[29] However, research by UK Finance finds the main motivating factor for households installing new technologies is cost savings.[30] So without the Government taking action to reduce the electricity-to-gas price ratio (which is currently 4:1), the green finance market will not be able to catalyse clean heat.[31],[32] The first paper in this Clean Heat series set out solutions to ensure electrification of heat delivers meaningful savings for customers.[33] The next paper will address how to improve consumer engagement and understanding of retrofit.

- Almost all available green home loans are secured (i.e. a form of mortgage), making them potentially unsuitable for the 45% of British homes that do not have a mortgage.[34] Although growing, the market for unsecured green home products is nascent, with a limited range of options compared to the green mortgage market. Growth has mainly been driven by not-for-profit lenders (e.g. community lenders and credit unions) and specialist lenders, with larger lenders entering the market more recently. These products typically include tight restrictions (such as using a certain manufacturer or installer) or have high interest rates.[35] Unsecured finance provided to individual borrowers in the UK is regulated by the Consumer Credit Act 1974 (CCA). Sections of the CCA have significant implications for the unsecured green home finance market, for example lenders can face uncapped liabilities if retrofits are poor quality.[36] Barclays suffered from this in the late 2010s after providing loans for solar panels, many of which were mis-sold.[37]

- Many green home finance products are loss-making due to low interest rates or cashback offers, so lenders would have to limit availability if demand were higher. For example, Nationwide notes it caps its 0% interest green additional borrowing product at 5,000 customers and will continue to do so without government support.[38]

The Government should invest £1.5 billion into subsidising a

range of commercial green home finance products to unlock up

to £9 billion of private consumer investment

Analysis by Energy UK shows that to increase the rate at which clean heating technologies are being installed in line with the CCC 7th Carbon Budget’s Balanced Pathway, around £9 billion to £10 billion of consumer-led investment is needed between now and 2030.[39]

Investing £1.5 billion of the £13.2 billion Warm Homes Plan budget into subsidising a range of commercial green home finance products could catalyse up to £9 billion of consumer investment.

Funding should be made available to lenders to subsidise a wide range of products, rather than focusing on one specific loan scheme, to allow lenders to meet the range of needs of their customers.

As well as supporting green additional borrowing and unsecured green home loans, the Government could also support nascent, innovative financing models including third-party ownership models, such as hire-purchase and conditional sale agreements, and ‘heat as a service’ – although this subscription model is only in its trial stages, and the Government should therefore carefully monitor the customer impacts of these models. There would also be value in exploring salary sacrifice schemes and property linked finance models.[40]

Energy UK supports third-party ownership agreements being allowed under the BUS, as this presents a range of ways for consumers to pay for clean heat.[41] Currently, the BUS does not allow third-party ownership because the regulations require the property owner to own the system once installed. A robust framework of consumer protections and advice on financial contracts is needed to support the fair implementation of these financing models.

The green finance subsidy should not, however, support green mortgages, as they reward already efficient homes rather than supporting new investments in clean heat and other low-carbon technologies.

Investment in a variety of home improvement measures – including heat pumps, heat batteries, heat network connections, solar panels, battery storage, and insulation – should be eligible for interest rate discounts. It should be possible to access subsidised products alongside government grants, such as the BUS.

The funding should target an average interest rate discount of around three percentage points. Secured loans have an average interest rate of 4%, while unsecured loans have an average interest rate of 6.5%.[42],[43] Implementing a blended average of three percentage points interest rate subsidy could deliver a 1.5% rate for mortgage linked products, and 3% rate for unsecured finance. To ensure that subsidised loans focus on supporting cost-effective investments, the Government should aim for an average loan length of 10 years, possibly with a 15-year limit on any loans. However, lenders should be required to support any borrowers that are struggling with repayments.

The Government should work with relevant stakeholders to deliver reform to the Consumer Credit Act to give lenders confidence to offer unsecured products

Reform to the CCA is complex, and collaboration across industry is key to overcoming the challenges it creates. One element of reform could be to require customers to provide evidence of seeking redress through the supplier before going to the lender, as advised by the European Consumer Credit Directive.[44]

Energy UK supports the proposals by UK Finance for the Government to deliver reform sensitively, so that vital consumer protections are retained while ensuring liability falls with those responsible for delivering poor-quality work.[45] The outcome of this reform should be that lenders are not dissuaded to offer unsecured products, and that consumers remain protected to the same degree they are now.

In the interim, while reform to the Act is being designed and agreed, the risk for lenders can be reduced by improving consumer protections, greater monitoring of quality standards, and a stronger programme of enforcement and redress among tradespeople in the retrofit sector. Energy UK will be exploring this in the next paper in its Clean Heat series.

The Government should align the tax regime with its targets for low-carbon technologies to further reduce the upfront costs

The tax regime for low-carbon technologies should be aligned with the Government’s ambitions to support the clean heat transition. This could further reduce the upfront costs for households, private landlords and businesses.

A key intervention should be to extend zero-rated Value Added Tax (VAT) on energy saving materials beyond the current end date of April 2027, to at least the end of 2030.

The Government should also consider other tax reforms, such as lowering business rates, which was explored in Energy UK’s business decarbonisation policy review and its 2023 publication ‘Small Business, Big Impact’.[46],[47]

How middle-income households can benefit from Government-subsidised green finance

Analysis by Energy UK of modelling by Cotality (Cotality UK provides data, insights, and workflows across the property ecosystem, see the appendix for more information) shows that allocating £1.5 billion of the £13.2 billion Warm Homes Plan budget into subsidising commercial green finance – from a typical 5% interest rate to a 2% rate – would help create access to clean heat and other low-carbon technologies, such as solar PV and batteries for up to 950,000 middle-income households by 2030.

Under a reduced Boiler Upgrade Scheme of £3,200, down from £7,500 – which Energy UK models as viable by 2030 in a scenario where the Government has implemented policy cost rebalancing and enabled a thriving green home finance market – a typical middle-income household taking out a £13,800 subsidised loan for a package of measures including an air source heat pump, solar PV array and a battery would save between £480 and £1,250 on their energy bills each year when they use energy flexibly.[48],[49],[50],[51] This range will vary according to the existing fuel used by the household and the baseline energy performance of the property. The potential benefits drop without rebalancing in place, with annual energy bill savings instead ranging between £320 to £830 after the three measures have been installed.

How a range of typical UK middle-income households could take advantage of subsidised green finance to reduce their energy bills

The following four case studies demonstrate how a range of typical middle-income households could benefit from affordable finance to install clean heat, and other low-carbon technologies, such as solar panels and a battery. This modelling, produced by Cotality for Energy UK, shows what the impact would be of an interest-rate subsidy programme on both secured and unsecured green home finance products.

The case studies demonstrate the additional benefits of introducing affordable green finance for low-carbon technologies in a scenario where policy cost rebalancing has been implemented, in line with the proposals set out in Energy UK’s ‘Balancing the bill’ paper, and which enables a corresponding reduction in the grant support available under the BUS from £7,500 to £3,200 by 2030.[52]

The modelling assumes that all homes with an existing gas boiler have an A-rated system, which means properties switching to clean heat from less efficient boilers would experience even greater energy bill savings.

The case studies assume that the household is using electrified heat and other low-carbon technologies flexibly to derive greater energy bill savings.

For more information on the modelling, see the appendix of this report.

Case study 1: Detached houses built between 1983 and 2001 (1,381,000 properties)

This household borrows either £9,500 to supplement a £7,500 BUS grant, or £13,800 in a rebalancing scenario to supplement a £3,200 BUS grant, over a maximum 10-year period to install an air source heat pump with radiators, a 3kWp solar PV array and a 10kWh battery.[53],[54],[55]

This household’s annual fuel bill of £3,083 can be reduced by 44% down to £1,726 through a combination of installing low-carbon technologies, using energy flexibly and rebalancing policy costs. Once the loan has been paid off, this household is paying half the price of their original energy bill in a rebalancing scenario.

For this property type, rebalancing enables the loan length for a secured product to be fewer than 10 years, which reduces costs for the household. It also enables the household to start benefitting from the energy bill savings generated by the technologies from the outset, with the household securing £10 in annual net savings during the length of the loan.

| Interest rate over a maximum 10-year loan length | |||||

| Secured | Unsecured | ||||

| 1.50% | 4% (no subsidy) | 3% | 6.5% (no subsidy) | ||

| No rebalancing £9,500 loan BUS grant of £7,500 | Total loan cost | £10,236 | £11,542 | £11,008 | £12,944 |

| Annual loan cost | £1,024 | £1,154 | £1,101 | £1,294 | |

| Annual benefit of interest rate subsidy | £131 | £194 | |||

| Annual energy bill savings | £795 | ||||

| Annual net savings during the length of the loan | -£229 | -£306 | |||

| Rebalancing £13,800 loan BUS grant of £3,200 | Total loan cost | £14,853 | £16,766 | £15,990 | £18,804 |

| Annual loan cost | £1,508 | £1,677 | £1,599 | £1,880 | |

| Annual benefit of interest rate subsidy | £159 | £234 | |||

| Annual energy bill savings | £1,518 | ||||

| Annual net savings during the length of the loan | £10 | -£81 | |||

Case study 2: Solid-wall terraced houses built before 1930 (2,866,500 properties in this profile):

This household borrows £9,500 to supplement a £7,500 Boiler Upgrade Scheme grant, or £13,800 in a rebalancing scenario to supplement a £3,200 grant, to install an air source heat pump with radiators, 3kWp solar PV array and a 10kWh battery.[56]

This household’s annual fuel bill of £2,586 can be reduced by 46% down to £1,396 through a combination of installing low-carbon technologies, using energy flexibly and rebalancing policy costs. Once the loan has been paid off, this household is paying half the price of their original energy bill in a rebalancing scenario.

| Interest rate over a maximum 10-year loan length | |||||

| Secured | Unsecured | ||||

| 1.50% | 4% (no subsidy) | 3% | 6.5% (no subsidy) | ||

| No rebalancing £9,500 loan BUS grant of £7,500 | Total loan cost | £10,236 | £11,542 | £11,008 | £12,944 |

| Annual loan cost | £1,024 | £1,154 | £1,101 | £1,294 | |

| Annual benefit of interest rate subsidy | £131 | £194 | |||

| Annual energy bill savings | £732 | ||||

| Annual net savings during the length of the loan | -£292 | -£369 | |||

| Rebalancing £13,800 loan BUS grant of £3,200 | Total loan cost | £14,869 | £16,766 | £15,990 | £18,804 |

| Annual loan cost | £1,487 | £1,677 | £1,599 | £1,880 | |

| Annual benefit of interest rate subsidy | £190 | £281 | |||

| Annual energy bill savings | £1,388 | ||||

| Annual net savings during the length of the loan | -£99 | -£212 | |||

Case study 3: Semi-detached houses and bungalows built between 1930 and 1983 (4,120,340 properties in this profile):

This household borrows £11,100 to supplement a £7,500 BUS grant, or £15,400 in a rebalancing scenario to supplement a £3,200 BUS grant, to install an air source heat pump with radiators, 3kWp solar PV array, 10kWh battery, and cavity wall insulation.[57]

For this property type, in a scenario where there is no rebalancing undertaken, including cavity wall insulation in the package of measures would improve the cost efficiency of the loan, as the amount saved would be more than the cost of the loan.

In the rebalancing scenario, the savings generated from the insulation are less because the energy bill is lower to begin with. This results in a lower annual benefit of the interest rate subsidy in a rebalancing scenario.

This household’s annual fuel bill of £2,365 can be reduced by 54% down to £1,088 through a combination of installing low-carbon technologies, using energy flexibly and rebalancing policy costs.

| Interest rate over a maximum 12-year loan length | |||||

| Secured | Unsecured | ||||

| 1.50% | 4% (no subsidy) | 3% | 6.5% (no subsidy) | ||

| No rebalancing £11,100 loan BUS grant of £7,500 | Total loan cost | £12,136 | £13,994 | £13,231 | £16,015 |

| Annual loan cost | £1,011 | £1,166 | £1,103 | £1,335 | |

| Annual benefit of interest rate subsidy | £186 | £278 | |||

| Annual energy bill savings | £894 | ||||

| Annual net savings during the length of the loan | -£117 | -£208 | |||

| Rebalancing £15,400 loan BUS grant of £3,200 | Total loan cost | £16,837 | £19,416 | £18,357 | £22,219 |

| Annual loan cost | £1,403 | £1,618 | £1,530 | £1,852 | |

| Annual benefit of interest rate subsidy | £258 | £386 | |||

| Annual energy bill savings | £1,382 | ||||

| Annual net savings during the length of the loan | -£21 | -£148 | |||

Case study 4: Electrically heated flats built between 1983 and 2023, older electric heating system (436,140 properties in this profile)

This household borrows £13,250 to supplement a £7,500 BUS grant, or £17,550 in a rebalancing scenario to supplement a £3,200 BUS grant, funding a connection to a shared loop individual ground source heat pump, 1.5 kWp share of PV array (part of a larger array whose power is shared between flats using a behind-the-meter solution), and a 5kWh battery.[58]

The share of PV array could be part of a larger array whose power is shared between flats using a behind-the-meter solution. This property may be better suited to alternative sources of funding for the communal measures, but this case study shows that these measures can also be funded on a household basis.

As this property is already on electric heating, it will benefit from rebalancing policy costs even without any uptake of additional measures. However, the combination of rebalancing and the installation of a modern electric heating system and supporting low-carbon technologies means that this household derives the greatest annual bill savings of the four case studies, once the loan has been paid off.

This household’s annual fuel bill of £2,615 can be reduced by 64% down to £941 through a combination of installing low-carbon technologies, using energy flexibly and rebalancing policy costs.

| Interest rate over a maximum 12-year loan length | |||||

| Secured | Unsecured | ||||

| 1.50% | 4% (no subsidy) | 3% | 6.5% (no subsidy) | ||

| No rebalancing £13,250 loan BUS grant of £7,500 | Total loan cost | £14,487 | £16,813 | £15,794 | £19,117 |

| Annual loan cost | £1,207 | £1,401 | £1,316 | £1,593 | |

| Annual benefit of interest rate subsidy | £194 | £277 | |||

| Annual energy bill savings | £1,380 | ||||

| Annual net savings during the length of the loan | £173 | £64 | |||

| Rebalancing £17,550 loan BUS grant of £3,200 | Total loan cost | £19,188 | £22,977 | £21,201 | £25,321 |

| Annual loan cost | £1,599 | £1,915 | £1,767 | £2,110 | |

| Annual benefit of interest rate subsidy | £316 | £343 | |||

| Annual energy bill savings | £1,655 | ||||

| Annual net savings during the length of the loan | £56 | -£111 | |||

Bringing down the cost of finance for heat network infrastructure

In addition to household finance, the Government should include support for bringing down the capital costs of heat network infrastructure within its Warm Homes Plan.

Heat networks are critical to delivering low-cost and low-carbon heat to households, businesses and public sector buildings in dense, urban environments. The heat networks sector has ambitions to invest £80 billion by 2050 in the development of new heat network infrastructure, promising significant regeneration benefits, and the creation of hundreds of thousands of new jobs and skills rooted in the communities they serve.[59] Heat networks benefit all energy customers by providing flexibility services to the grid, which helps to improve the resilience of the energy system and bring down system costs.

Investing in the development of new, low-carbon heat network infrastructure is a long-term prospect. Investment cycles of 20-25 years account for the build time, and for the network to become operational and profitable as customers connect.

Investors that can take a sufficiently long-term view also tend to be risk averse. However, large city-wide heat networks are effectively a nascent sector in the UK. The regulatory approach to heat network zoning is still in development and blockers within the planning system need to be resolved. Energy UK will address this later in its Clean Heat report series.

Securing demand for heat network supply can also be challenging due to the high price of non-domestic electricity relative to gas. The Government should prioritise addressing the high relative cost of electricity, with a strong commitment in the Warm Homes Plan to a temporary revenue support model that tackles the cost of heat in the near term, ahead of the rebalancing of policy costs on non-domestic energy bills.

These barriers affect the investment prospect for new heat networks, as the risk is higher, pushing up the cost of development capital, and ultimately the cost to customers that connect.[60]

To support the build out of new heat networks at scale, the Government has a key role to play in removing barriers to heat network development and bringing down the cost of capital.[61] The Warm Homes Plan is an important opportunity to de-risk investment through the continuation of grant support. The plan should also aim to give heat network developments access to low cost debt financing, which the sector currently struggles to secure due to the risk associated with revenue typically being generated late in the investment cycle. Lower cost debt would help to reduce the development cost and drive down the end cost to the consumer.

The Government should allocate £485 million to the Green Heat Networks Fund (GHNF) under the Warm Homes Plan

The continuation of grant support will increase the heat network sector’s confidence to invest in new development and enhance the capability and capacity of the supply chain, helping reduce risk for investors.[62]

The Government should confirm the allocation of £485 million for the GHNF under the Warm Homes Plan.[63]

To help address the challenge of connection costs – and thereby help address the risk of demand assurance – the Government could introduce greater flexibility into the GHNF by bringing connection costs in scope of the grant, and in particular public sector connections. Following the Government’s decision to discontinue the Public Sector Decarbonisation Scheme beyond 2028, this would help to bridge the gap in support for public sector energy customers for the remainder of this Parliament, and ensure that they, and the supply chains serving them, do not face a cliff-edge in terms of support to reduce energy bills while delivering on decarbonisation objectives.

The NWF should guarantee a package of commercial development loans for projects that have successfully acquired funding through the GHNF

The NWF has a strategic direction to focus on the delivery of clean heat and could play an important role in addressing the cost of capital for heat network infrastructure. The sector struggles to access cheap debt financing because it is expensive to service, and revenue from heat networks is typically generated later in the investment cycle. The NWF can help networks overcome this by cutting the cost of debt, which would lower development costs and ultimately reduce costs to customers that connect.

The NWF already provides guarantees to commercial lenders to support lower cost lending to projects that deliver growth and tackle climate change, such as the £1.3 billion in guarantees for loans to social housing providers investing in decarbonisation.[64] The NWF should seek to replicate this arrangement for lending for heat network development, by streamlining access to finance offering guarantees to lenders for projects that have been awarded funding through the GHNF. Focusing on GHNF backed projects will provide quality assurance to de-risk NWF’s investment.

The NWF should lend to combined authorities with regional energy strategies in place, to fund public-private partnerships delivering area-based retrofit

The NWF has £4 billion to provide low-cost finance to regional government delivering capital-intensive projects across the UK. It has already taken steps to support local authorities with heat decarbonisation initiatives – for example by providing low-cost, long-term financing to Solihull Metropolitan Borough Council to enable the council (and delivery partner Vital Energi) to deliver the first phase of a heat network in the city.[65]

The NWF can go further by utilising its strategic partnerships with combined authorities to deliver area-based solutions to heat decarbonisation, by lending to these combined authorities where they are working in partnership with the private sector, through a competitive procurement process, to deliver strategic energy infrastructure. For example, the West Midlands Combined Authority (WMCA) has a Regional Energy Strategy in place following its ‘Deeper Devolution Deal’ with the UK Government – a single integrated settlement including retrofit funding and new powers on energy and Net Zero.[66],[67]

Building on this settlement, the WMCA has a remit to explore innovative financial models to overcome barriers to retrofit. This could include aggregating demand and accessing low-cost finance from the NWF to deliver place-based, multi-asset class retrofit programmes in partnership with the private sector. This would include heat networks, but as pilot schemes such as the Nesta ‘Clean Heat Neighbourhoods’ scheme has shown, it could be extended to other technologies to provide a range of solutions for communities.[68]

Aggregating demand in this way would enable the combined authority to distribute finance to individual non-domestic customers, such as hotels or leisure centres, that need support with the upfront capital cost of connecting to a heat network but are unable to access help through the NWF due to its minimum ticket size of £25 million.[69] Helping businesses such as these make the switch to low-carbon, efficient heating through heat networks would reduce their energy costs and, in turn, costs to consumers. It would also protect connected businesses and other buildings from volatile energy prices.

Conclusion

As highlighted in the first paper of this clean heat series, the price of electricity needs to be reduced in order to drive uptake of low-carbon technologies, including clean heating systems.[70] Intervention is also needed to bring down the upfront capital costs of the clean heat transition for households and businesses. Low-cost loans are a crucial piece of the puzzle for the Government’s Warm Homes Plan, to make sure that households of all income levels can benefit from low-carbon technologies that reduce energy bills, deliver growth and bolster the UK’s energy security.

The Government should commit £1.5 billion of its Warm Homes Plan to subsidise commercial green finance products to unlock up to £9 billion of private consumer investment into the clean heat transition. This would support up to 950,000 households to upgrade their homes.

Modelling by Cotality for Energy UK shows that households living in properties that are typical of those on middle-incomes can lower their energy bills by accessing subsidised green finance, installing a cost-effective package of measures and using energy flexibly in a scenario where policy costs have been rebalanced.

To bring down the capital costs of heat network infrastructure, the Government should encourage investors by continuing support for the Green Heat Network Fund as part of its Warm Homes Plan. The NWF also has a key role to play in supporting heat network development. It can do this by providing guarantees for debt finance for these developments, and offering affordable finance to combined authorities implementing regional energy strategies in partnership with the private sector.

Appendix

About this series

This is the second of Energy UK’s Clean Heat series of policy reports, which aim to show how the transition to clean heat can be delivered in a way that lowers bills for energy customers and boosts economic growth, jobs and skills across the country. Other reports in the Clean Heat series will explore the themes of finance, regulation, jobs and skills, and consumer engagement and protections.

To discuss this series –or any of our analysis – in more detail, please email press@energy-uk.org.uk or louise.shooter@energy-uk.org.uk.

About Cotality UK

Cotality provides data, insights, and workflows across the property ecosystem, supporting property marketing, insurance, lending and retrofit. With billions of data signals across the life cycle of a property, Cotality identifies risks and opportunities for agents, lenders, insurers, governments, homeowners and innovators.

In the energy sector Cotality provides quality assurance and obligation-handling services for the delivery of ECO, and stock modelling for landlords, local authorities and lenders to identify the need and opportunity for retrofit at scale. To reduce barriers to homeowners, Cotality’s One Stop Shop services – including detailed online advice, and independent retrofit assessment and coordination – are available nationally delivering direct to homeowners or via partners. Find out more at cotality.com/uk.

About the case study analysis

Energy UK asked Cotality to assess the potential scale and impact of finance options that could support the rollout of clean heat. With a need for detailed scenario testing and illustrative, representative examples, using archetypes offered a route to in-depth analysis that would reflect the opportunity in the wider housing stock.

Cotality identified homes representative of the four dominant archetypes in the UK housing stock: detached houses built between 1983 and 2001, solid-walled terraced houses built before 1930, semi-detached houses and bungalows built between 1930 and 1983, and electrically heated flats built between 1983 and 2023. It then identified the most cost-efficient measures relevant to the homes to deliver clean heat without increasing bills. These packages were generated by Cotality’s recommendations engine with cost estimates based on the detail of each home. This analysis provided an installation cost and resultant annual energy use, which enabled the calculation of a payback period – how long it will take to pay back the installation cost from the reduced energy use. Additional scenario analysis then enabled consideration and comparison of different policy options that would affect this payback, including rebalancing policy costs, inclusion of different measures (heating, solar, storage and insulation), potential interest rate options and payback periods.

[1] UK Government (2025), Spending Review

[2] Resolution Foundation (2024), Net Zeroing in on investment

[3] More in Common (2025), Doom Loop Deepens

[4] Energy UK (2025), Clean Heat: Balancing the bill

[5] UK Government (2024), Evaluation of the Boiler Upgrade Scheme

[6] The exact number of households benefitting would depend on the type of properties and the number of measures taken up.

[7] MCS (2025), Homeowner attitudes to retrofit finance

[8] Energy UK (2025), Energy UK Explains: Heat networks

[9] UK Government (2023), Green Heat Network Fund: full business case

[10] MCS (2025), The MCS Data Dashboard

[11] Climate Change Committee (2025), Seventh Carbon Budget

[12] UK Government (2025), UK Heat Networks: Market Overview

[13] Climate Change Committee (2025), Seventh Carbon Budget

[14] We use the 2024-2025 increase in installations to determine to uptake rate year on year from 2026 to 2030.

[15] Energy UK (2025), Clean Heat: Balancing the bill

[16] Energy UK (2025), Reducing non-domestic electricity prices to drive economic growth – Energy UK

[17] Climate Change Committee (2025), Seventh Carbon Budget

[18] It should be noted that subsequent technology replacements will be lower, or in the case of a heat network, not necessary.

[19] UK Government (2025), Help from your energy supplier: the Energy Company Obligation

[20] UK Government (2025), Warm Homes: Social Housing Fund Wave 3

[21] UK Government (2025), Boiler Upgrade Scheme statistics

[22] UK Government (2024), Evaluation of the Boiler Upgrade Scheme

[23] The Labour Party (2024), Change

[24] British Gas (2025), Air source heat pumps

[25] T&Cs Apply. Sunsave act as a credit broker, not a lender. Credit is subject to status and checks. Full details available on the Sunsave website.

[26] Octopus Energy (2025), Solar

[27] Halifax (2025), Heat pumps

[28] Kensa (2025), Ground Source Heat Pump funding

[29] MCS (2025), Attitudes to Retrofit Finance

[30] UK Finance (2025), Greening Homes, Creating Growth

[31] Ofgem (2025), Energy price cap

[32] UK Finance (2025), Greening Homes, Creating Growth

[33] Energy UK (2025), Clean Heat: Balancing the bill

[34] ONS (2021), Household characteristics by tenure, England and Wales; Bank of England (2023) The buy-to-let sector and financial stability

[35] Green Finance Institute (2024), Unsecured Green Home Loans

[36] Green Finance Institute (2024), Unsecured Green Home Loans: Demystifying the Market

[37] BBC (2019), Solar panels: Thousands of customers complain

[38] Nationwide (2024), How low-cost finance supports the greening of UK homes

[39] The required spend by 2030 for CCC’s low-carbon heating and energy efficiency from which government schemes budgets are deducted (WHP + ECO + GBIS). We assume that ECO will be extended and include GBIS budget until 2029.

[40] Green Finance Institute (2024), A greenprint for Property Linked Finance in the UK

[41] Energy UK (2025), Boiler Upgrade Scheme and certification requirements for clean heat schemes

[42] MoneySuperMarket (2025), Mortgages

[43] Santander (2025), Personal loans

[44] European Union (2008), Directive – 2008/48 – EN – consumer credit directive – EUR-Lex

[45] UK Finance (2025), ’Greening Homes, Creating Growth’

[46] Energy UK (2025), ‘Review of policies to drive commercial and industrial decarbonisation’

[47] Energy UK (2023), Small Business, Big Impact

[48] Energy UK (2025), Clean Heat: Balancing the bill

[49] This loan size deducts the cost of a boiler to account for the opportunity cost of not having to install a new one (i.e. £3,000)

[50] Flexible tariffs are assumed to be 20% lower than price cap rates. We assume that household taking-up heat pumps will be disconnected from gas. Price cap rates refer to current rates.

[51] Energy bill savings figures apply to houses having upgrades made, but the range would be different for flats.

[52] Energy UK (2025), Clean Heat: Balancing the bill

[53] The size of the loan takes away the cost of the boiler (i.e. £3,000) to account for the opportunity cost. We assume that a middle-income household would have contracted a loan to replace its boiler.

[54] The loan is limited to 10 years when it is not cheaper to finance it under 10 years (i.e. where annual savings are not sufficient to service the total cost of loan under 10 years).

[55] Kilowatts peak (kWp) measure the generation of solar panels at peak performance.

[56] The size of the loan nets off the cost of the boiler (i.e. £3,000) to account for the opportunity cost. We assume that a middle-income household would have contracted a loan to replace its boiler.

[57] The size of the loan nets off the cost of the boiler (i.e. £3,000) to account for the opportunity cost. We assume that a middle-income household would have contracted a loan to replace its boiler.

[58] The size of the loan nets off the cost of the boiler (i.e. £3,000) to account for the opportunity cost. We assume that a middle-income household would have contracted a loan to replace its boiler.

[59] UK Government (2024), UK Heat Networks Market Overview

[60] Energy UK will explore further how regulation can drive growth in a future paper

[61] UK Government (2025), Heat Network Zoning Pilot

[62] UK Government (2023), Full Business Case for Green Heat Network Fund GHNF

[63] UK Government (2023), Full Business Case for Green Heat Network Fund GHNF

[64] UK Government (2025), Social rented housing: Repairs and maintenance: Question for Treasury

[65] National Wealth Fund (2025), Financing the Future

[66] West Midlands Combined Authority (2023), Trailblazing Devolution for the West Midlands

[67] West Midlands Combined Authority, Regional Energy Strategy

[68] Nesta, Clean Heat Neighbourhoods

[69] National Wealth Fund, Our Products and Terms

[70] Energy UK (2025), Clean Heat: Balancing the bill

Downloads

-

Energy UK – Clean Heat – Financing the transition

Type: PDF (532 KB)