Energy is essential to our daily lives and in a changing global environment, the need to secure our future energy resources is fundamentally reshaping our energy system.

The UK has made remarkable progress in transforming how we generate electricity. From removing over 80% of emissions from the power sector since 1990, to phasing out coal, and building over 60GW of renewables. But realising the benefits of clean power will require looking beyond energy generation, right through to energy supply.

The focus must now be on how we make it easier for households and businesses across the country to unlock the benefits of flexibility services, technology adoption, and dynamic pricing – capabilities and markets which take years to build.

The Energy UK and BFY Group report Demand better: A smarter, fairer energy retail market makes the case for a reset and reimagined retail energy market that will unleash an innovative, competitive, and thriving sector that not only supplies affordable, abundant clean power but also improves customer experience and strengthens consumer protections.

The future role of the retail market

The case for retail market reform extends far beyond consumer protection or competition. At stake is Britain’s ability to achieve its clean energy ambitions, deliver economic growth and maintain energy security. Energy suppliers are not passive observers of the transition happening in energy generation. They are the businesses that will invest, innovate and develop the solutions that will ultimately determine whether decarbonisation targets remain achievable or slip beyond reach.

Government’s policy ambition is to decarbonise the power sector by 2030 and deliver successive carbon budgets that reduce emissions to Net Zero within the next 25 years. Central to this is the delivery of the Clean Power Plan, with expanding renewable generation, the electrification of heat and transport, increased demand flexibility and digitalisation as the four key pillars supporting the transformation. Each of these pillars is dependent on a well-functioning retail market.

The retail market and the operating environment for energy suppliers at present is not set up to do this:

- Customer debt and focus on survival consume resources which should be spent creating the products and services that could reduce bills and improve customer outcomes.

- Housing tenure, income, and digital barriers make it harder for large parts of the population to actively participate in the energy market.

- The burdensome policy and regulatory environment for the retail market cripples innovation, stifles investment, and is prone to performative interventions that do little to support better long-term outcomes.

- The price cap was introduced to protect customers being overcharged as a result of their choice not to engage with the energy market and switch to a better deal, for example fixed or flexible tariffs. Over half of all households are now on the price cap. The result is energy suppliers operating in a market with compressed margins and unengaged customers where uncertainty is high and returns do not justify the risk.

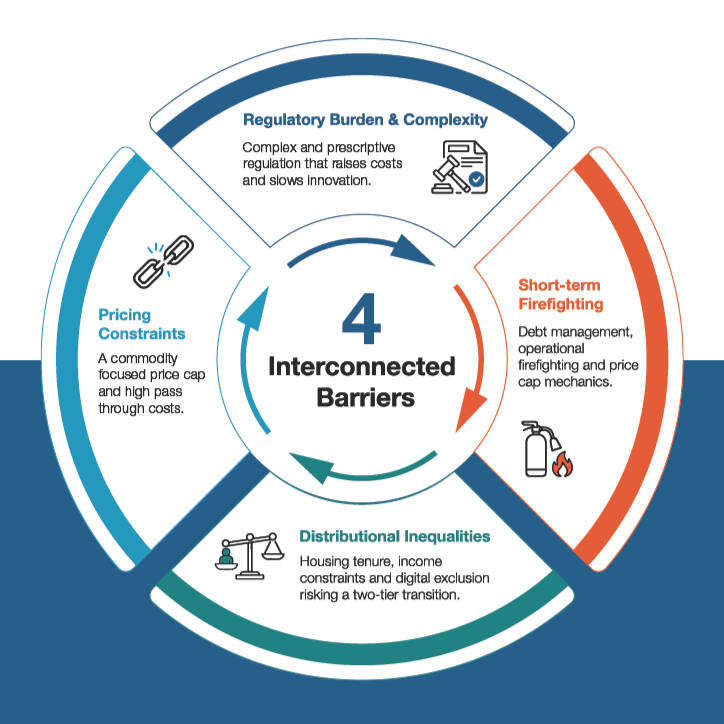

Barriers and solutions to a smarter, fairer retail market

First, regulatory burden and complexity has reached unsustainable levels. Supply licence conditions and industry codes now span nearly 10,000 pages of excessively prescriptive requirements. Ofgem’s preference for input-based regulation mandates specific systems and processes, deterring investment. Business model innovation becomes difficult when licence conditions assume

ways of working that were relevant at a time when the retail market meant commodity supply rather than integrated service provision.

Second, short-term firefighting crowds out long-term investment. Household energy consumers owe energy suppliers £5.5bn and rising,7 creating a growing crisis that is consuming substantial resource. Price cap mechanics require ongoing attention towards hedging, forecasting and regulatory engagement. These immediate needs absorb management time and capital that would otherwise be innovating around the development of the propositions and partnerships we need for the future.

.

Third, distributional inequalities create structural barriers that retail propositions alone cannot overcome. Housing tenure limits the ability of 5.4 million private rental households from installing technology such as heat pumps or EV chargers regardless of how attractive retail offers become. Income constraints place low

carbon technologies beyond millions of people’s reach. Digital exclusion affects approximately 3.1 million households lacking internet access, with at least 2 million more facing barriers from inadequate devices, unaffordable data or poor digital skills. Without addressing these barriers, the transition risks creating a two-tier

system where benefits flow to affluent early adopters while costs fall on those unable to participate.

.

Fourth, pricing constraints severely limits innovation. The commodity-focused price cap restricts the development of and demand for the dynamic tariffs, time-of-use pricing and bundled services essential for flexibility. Over 50% of the bill is made up of pass-through charges suppliers cannot influence. When suppliers lack pricing power over most of the bill, their ability to design compelling propositions is limited.

.

Policy solutions

Regulation that is outcomes focused, accessible and not burdensome

- Government must provide a clear and strategic direction that the aim of regulation should be to enable investment and innovation while maintaining essential consumer protection.

- There should be a comprehensive supply licence review, with a binding commitment to reduce regulatory burden and refocus on consumers, investment and modernising the energy system.

- Sunset principles should be introduced so input-based obligations must justify their continuation rather than assuming persistence by default.

- Outcomes-based standards should be designed collaboratively with industry and consumer advocacy groups. These standards should be measurable, achievable and genuinely linked to consumer benefit.

A regulatory framework set up to expand flexibility markets

- Regulation should apply to services, not business types, with a level playing field across all market participants offering each service.

- Light-touch licensing for flexibility service providers, including suppliers acting in this capacity, should be finalised and introduced as soon as possible.

- Industry codes should be modified to establish formal interaction protocols between suppliers and flexibility service providers.

- Flexibility service providers and energy suppliers should be granted clear rights to half-hourly consumption data and asset performance metrics, subject to consumer consent.

- Regulatory burden reduction should target specific compliance areas including licence condition simplification, streamlined reporting requirements and removal of prescriptive operational mandates that impose costs without protecting consumers.

Debt and affordability must be addressed as a priority

- Ofgem should establish a sustainable debt management framework, building on the Debt Relief Scheme and combining mechanisms to address existing debt for consumers genuinely unable to pay with improved regulatory tools that prevent the accumulation of debt.

More certainty to industry and avoid knee-jerk policy making

- The Department for Energy Security and Net Zero (DESNZ) should set out strategic priorities for retail market reform through the Strategic Policy Statement focused on the medium to long-term priorities needed to deliver policy aims.

- Ofgem, the energy regulator, should conduct a formal impact assessment before starting any work that sits outside its planned forward work programme, with a high threshold to be cleared before resource is committed.

Upgrades to customer infrastructure

- Government should mandate minimum energy performance standards for rental properties and when upgrading government buildings, requiring landlords and governmental bodies to install smart meters, EV charging infrastructure where possible and practical, and low-carbon upgrade sat point of major refurbishment.

- On-bill financing schemes should be supported, enabling households to adopt EVs, batteries and heat pumps without upfront capital, repaying through energy savings over equipment lifetimes.

- Network cost recovery should shift from volumetric charges to capacity-based standing charges, ensuring households with solar and batteries remaining connected for resilience bear appropriate network costs.

- Address digital exclusion with rural broadband investment, and regulatory requirements so that energy services remain accessible through phone and post for those unable to use digital channels.

- Government and industry should work together on the plan for the tail end of the smart meter rollout, requiring all new buildings to be compatible with smart meters, and planning for the gradual phasing out of the legacy metering infrastructure.

.

Evolving price protection

- Ofgem should publish a multi-year roadmap for the evolution of the price cap, specifying whether protection will narrow, transition to social tariff models, or remain universal, enabling suppliers to plan investment accordingly.

- Price protection must transition away from universal coverage to targeted support for those genuinely unable to engage or afford energy, with tariffs exempted where consumers opt in with informed consent.

- Bundled services that combine equipment and energy should receive separate regulatory treatment, assessing overall value proposition.

- Time-of-use tariffs should be allowed to preserve meaningful peak-to-off-peak differentials to maintain incentives for shifting demand.

Pricing frameworks designed to minimise/optimise energy costs and support the system

- Reformed national pricing must deliver a more cost-effective energy system to enable suppliers to design tariffs that reflect true system value.

- Policy cost allocation must shift away from electricity bills toward progressive funding mechanisms such as taxation, building on the Renewables Obligation announcement in the 2025 Budget.

If you require this report in a different format please contact press@energy-uk.org.uk

Downloads

-

Demand Better-A smarter fairer energy retail market – April 2026

Type: PDF (1 MB)