In the wake of the energy crisis, the Government has a crucial opportunity to unlock the potential of the retail energy market, support customers who need help, and encourage the green shoots of growth the sector is already seeing.

You’ll find an accessible version of the report below. For accessible versions of the graphs included in the PDF document, contact us.

Executive summary

Energy is an essential service. The Government has a crucial opportunity to unlock the potential of the retail energy market following the energy crisis, refocusing interventions to better support households that need help, and encouraging the green shoots of growth that we are already seeing. With clear policy direction and proportionate regulation, opportunity can be seized for the benefit of consumers.

We have an affordability challenge of higher prices and debt levels hitting households, constraining their ability to save and to spend, and impacting health outcomes. It is especially acute in winter because cold homes have very real impacts on health and wellbeing; the health consequences alone cost the NHS c. £2.5 billion per year.[1],[2],[3]

The regulator and energy suppliers cannot address affordability on their own. In this paper, Energy UK has set out how the Government can approach this for the coming winter alongside the essential work necessary for a fairer, more sustainable solution to targeted support.

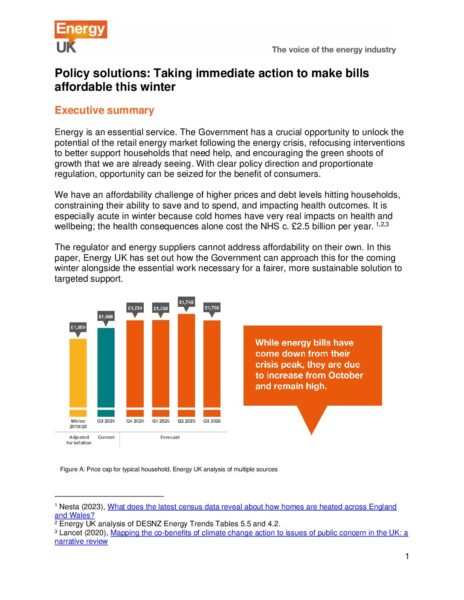

While wholesale prices have come down from their crisis peak, the price cap is set to increase from 1 October 2024, with a likely increase of around 10% from the current £1,568 to £1,723.06.[4] The trend is for cap rates to hold at around this higher number. Ofgem will be publishing the actual cap rates on 23 August 2024.

Household debt levels are also increasing, with millions of households facing unaffordable bills. Ofgem has put the overall debt level for domestic customers at £3.32 billion, although this is likely to be a significant underestimate.[5] National Energy Action has highlighted that there are around 6 million households struggling with fuel poverty overall.[6] We can see this very worrying trend in Figure B below.

This aggregate number is significant but doesn’t show the very real scale of debt per impacted household. Where customers have no payment plan in place, the average debt level now (Q1, 2024) stands at £1,452 for electricity and £1,264 for gas. This is an annual increase of 19% and 31% respectively.

This causes huge anxiety for customers struggling with debt and disproportionately affects those on lower incomes.[7] This is reinforced by data from Citizens Advice, which is seeing an increase in calls from customers who struggle to pay their energy bills, with energy debt being the biggest call driver.[8] The organisation puts the average energy debt owed by its clients at £1,835 by the end of 2023, which is up from £1,579 a year earlier. Customer debt is clearly going in the wrong direction.

Recent Office of National Statistics data builds on this by showing direct debit failure is increasing month on month across a range of key household costs, including energy.[9]

Our proposals for reform

Taken together, Energy UK believes this package of reform could have an immediate and sustained effect for bringing down the price of energy for households across the country. Working with industry, the Government needs to implement the following:

- Fund Energy Company Obligation (ECO) and Great British Insultation Scheme (GBIS) through Government spending. This will have a cost of c.£1.5 billion per year. This could potentially be classified as capital spending, which may help with fiscal rules.

- Move remaining policy costs onto gas bills, to a ratio of electricity to gas prices of around 3:1. This will have a key benefit of ensuring low-carbon technologies are cheaper to run than fossil fuel alternatives.

- Funding ECO and GBIS will free up sufficient room on the energy bill to enable a doubling of the Warm Home Discount (WHD) support for the most vulnerable households for winter 2024.

- Taken together, an expanded WHD and policy cost rebalancing could support households and reduce bills. Households with electric heating could save up to £400 per year, or up to £550 for those eligible for WHD.

- Instigate a cross-departmental Director General-led working group on data and data access needed to support long term targeted bill support from winter 2025.

Introduction

Wholesale energy costs have fallen considerably since the peak of the gas crisis. However, prices remain some 50% (in nominal terms, 25% when adjusting for inflation) higher than pre-crisis levels, which leaves millions of households facing unaffordable bills. Prices also remain volatile, and with household energy debt now standing over £3.1 billion (which is likely to be a significant underestimate) resilience to future shocks is extremely low.

Energy suppliers spend tens of millions of pounds a year on discretionary support for customers.[10] Ofgem has introduced new regulatory protections, but only the Government can ultimately solve the affordability crisis. There is a clear need for longer-term work on targeted support, utilising government and industry data on households’ income and energy needs to ensure that the Government has the means to protect the most vulnerable households. In the short term, the existing level of £150 Warm Homes Discount (WHD) is inadequate in the face of current prices and needs to be increased and extended to more households.

Prices are not just high, they are also a major barrier to the Net Zero transition. It will be important for the Government to be able to show that ambition on low-carbon generation is matched by bills starting to fall. Policy costs on bills now account for almost £200 (£188) per typical household per year.

Worse, these policy costs fall disproportionately on electricity bills, resulting in a major disincentive for customers adopting low-carbon technologies such as Electric Vehicles (EVs), heat pumps and batteries. This distortion is on top of the fact that electricity faces a significant carbon price through the UK Emissions Trading System (ETS) and Carbon Price Support, while gas does not. In the longer term, a carbon price on gas through either an ETS or standalone tax would help to address this distortionary imbalance.

Solutions

This paper outlines the urgent actions the next Government needs to take to improve support for vulnerable households, start bringing down bills and incentivising Net Zero technologies while keeping costs to the taxpayer modest. The Government could achieve this by taking three steps:

- Reduce the burden of policy costs on bills

- Rebalance the remaining costs on bills

- Improve targeted support.

Reduce the burden of policy costs on bills

Currently, policy costs on domestic bills total around £5 billion per year, paying for now-closed legacy schemes to incentivise renewables, such as the Renewables Obligation (RO) and Feed in Tariffs (FiT), alongside existing schemes to improve housing energy efficiency, including the Energy Company Obligation (ECO) and Great British Insulation Scheme (GBIS). This is alongside direct support to reduce bills of the poorest households through the Warm Home Discount (WHD).

The fastest way to bring bills down is to fund some existing policy costs through general Government spending. Paying for policy costs through bills is highly regressive, as poorer households spend a greater proportion of their income on energy.

Funding the legacy costs associated with the old RO and FIT schemes would cost Government around £3 billion a year which starts to fall from 2027 as the schemes’ liabilities wind down. If this is considered fiscally unaffordable, then providing Government funding for ECO and GBIS could be done at a cost of £1.5 billion a year and could potentially be classified as capital spending which may help with fiscal rules. This could be achieved either by moving the funding for ECO and GBIS into Government spending, or by providing a rebate to customers that reflects the full amount of these schemes which totals around £1.5 billion.

This has been done before through mechanisms such as the Energy Price Guarantee (EPG) and Government Electricity Rebate. Either solution must be implemented with care to ensure that the operation of ECO and GBIS is not disrupted by such a policy, and that there is no need for new delivery mechanisms or public procurement processes given that such structures already exist.

Funding a portion of existing policy costs through general Government spending would result in immediate bill reductions for all households. It could also facilitate some other policy choices that would see future bill increases, for example increasing the size of WHD or introduction of new levies for hydrogen/Carbon Capture, Utilisation and Storage (CCUS) or nuclear.

Rebalance the remaining costs on bills

Any policy costs remaining on bills should be spread more fairly and be better aligned with Net Zero aims. This could be achieved by implementing a rebalancing levy that shifts a proportion of domestic policy costs remaining on electricity bills to gas.[11] This should aim to achieve a ratio of electricity to gas prices of around 3:1 which will ensure low-carbon technologies are cheaper to run than fossil fuel alternatives.

Approaching this through a rebalancing levy would also enable the next Government to adjust to any future changes in costs (for example new levies or falling numbers of gas users) while maintaining incentives towards Net Zero. While this paper is concerned with domestic prices, a similar approach could be used to rebalance non-domestic prices too.[12]

Such a move would result in a small increase in bills for households that use gas for heating due to there being fewer gas customers than electricity customers; meaning the levy would result in a slightly larger increase in gas bills than fall in electricity bills. However, this impact would be small in comparison to the reduction in bills achieved in step one. Implemented correctly, no low-income household would be worse off, including those who continue to use gas for heating.

Improve targeted support

Steps one and two will result in lower bills for the vast majority of households. However, paying for energy will still remain unaffordable for many. Whilst there is a clear need for better targeted and enhanced support for vulnerable households, the quickest and most pragmatic way to improve short-term support is through reform of the WHD, whilst giving time for the Government to shift the dial on the data needed to enable targeted support.

The current support, providing £150 per year, is lower than the typical household pays in policy costs. To offer serious protection this amount should be at least doubled for the most vulnerable households. Further, it should be provided to more households, potentially on a tiered basis (so for example a core group of recipients get the full discount and a wider group get a reduced discount).

As a social policy, WHD would be considerably more progressive if funded through general Government spending. However, Energy UK’s calculations show that if the Government was to fund £1.5 billion of policy costs through step one, then funding a doubling of WHD through bills could be achieved without increasing the average household bill in aggregate.

By winter 2025, the Government will need to look more fundamentally at the appropriateness of bill support for a new, more volatile outlook. Affordability and debt are already acute issues in the sector and are challenges that will be exacerbated in the event of further market turbulence. If a future price spike were to create the need for large-scale bill support then the Government currently does not have a mechanism capable of targeting support at a greater level and so would need to use extremely expensive universal measures, such as the EPG, again.

Energy UK analysis based on Ofgem’s energy consumer archetypes shows this was ineffective in providing relative support according to need, with some of the richest households receiving the most support. This blanket approach was therefore an inefficient use of tax-payer money.

The Government should look urgently to set up a cross-Whitehall project to develop data access and matching to enable targeting of future bill support. The lack of such data and its availability has led to the adoption at speed of universal schemes or other pragmatic proposals. However, drawing on precedents from Covid-19 and the energy crisis for example, delivery could be expedited through a project led by a DG from a relevant department (DESNZ/HMT/DWP/HMRC), charged with coordinating across Whitehall, and with a dedicated budget (recognising that technical work will be required to achieve this). This role should be introduced with the expectation of completion in time for winter 2025.

In parallel, Government should work with charities and suppliers to develop a framework for targeting support to those who would need it most were such a future crisis to materialise, which would align with opening up access to the data needed to support households that need it most.

Our proposals for reform

Taken together, Energy UK believes this package of reform could have an immediate and sustained effect for bringing down the price of energy for households across the country. Working with industry, the Government needs to implement the following.

- Fund Energy Company Obligation (ECO) and Great British Insultation Scheme (GBIS) through Government spending. This will have a cost of c.£1.5 billion per year. This could potentially be classified as capital spending, which may help with fiscal rules.

- Move remaining policy costs onto gas bills, to a ratio of electricity to gas prices of around 3:1. This will have a key benefit of ensuring low-carbon technologies are cheaper to run than fossil fuel alternatives.

- Funding ECO and GBIS will free up sufficient room on the energy bill to enable a doubling of the Warm Home Discount (WHD) support for the most vulnerable households for winter 2024.

- Taken together, an expanded WHD and policy cost rebalancing could support households and reduce bills. Households with electric heating could save up to £400 per year, or up to £550 for those eligible for WHD.

- Instigate a cross-departmental DG-led working group on data and access needed to support a long term targeted bill support from winter 2025.

For more information or to discuss this briefing contact Alexander.Gray@energy-uk.org.uk

Annex: Details of policy costs

| Scheme | Cost per typical bill | Total cost | Purpose | Future trajectory |

| Renewables Obligation (RO) | £86 on electricity | £3bn | Funding the previous generation of investment in large-scale renewables (e.g. onshore and offshore wind). | The schemes are closed and the level of support will taper away over the next two decades from 2027. |

| Feed-in Tariffs (FiT) | £21 on electricity | £0.75bn | Funding the previous generation of small-scale renewables (e.g. solar panels on roofs). | |

| Energy Company Obligation (ECO) and Great British Insulation Scheme (GBIS) | £23 on electricity £35 on gas | £1.5bn | Funding the installation of energy-efficiency measures for low-income households. | Steady, unless there are policy changes. |

| Warm Homes Discount (WHD) | £11 on electricity £11 on gas | £0.5bn | Providing annual payments of £150 to eligible low-income households to support them with energy costs. | |

| Contracts for Difference | Variable, depending on market conditions | The current scheme to support the development of renewables by offering fixed-price contracts with generators that provide price stability for consumers. | The volume of CfDs will increase rapidly over time with the average price falling. This will have the effect of making electricity costs more stable for consumers. | |

| Others | Negligible | Funding things like support for high network costs for remote households and producing green gas. | Not material. | |

| Potential new programmes | To be decided | There have been proposals to fund support developments like hydrogen, CCUS and the decommissioning of the gas grid. | Depending on what decisions are made, will ramp up over the next five years/decade. | |

[1] Nesta (2023), What does the latest census data reveal about how homes are heated across England and Wales?

[2] Energy UK analysis of DESNZ Energy Trends Tables 5.5 and 4.2.

[3] Lancet (2020), Mapping the co-benefits of climate change action to issues of public concern in the UK: a narrative review

[4] Cornwall Insight (accessed 18/07/24), Predictions and Insights into the Default Tariff Cap

[5] Ofgem (June 2024), Debt and Arrears Indicators, Q1 2024

[6] NEA (2024), Price cap is falling, but 5.6 million UK households continue to struggle with energy bills

[7] ONS (2022), Energy prices and their effect on households

[8] Citizens Advice (2024), Shock Proof

[9] ONS (2024), Monthly Direct Debit failure rate and average transaction amount

[10] Energy UK (2024), Additional support for customers

[11] RO and FiTs are well-established schemes with a strong legal foundation. It may be practically simpler to maintain the existing structure of the programmes as much as possible with funding for the domestic component switched to a dedicated levy on gas.

[12] Rebalancing should be considered separately for domestic and non-domestic customers for two reasons:

- Households consume a larger proportion of gas (over half) than electricity (around a third), meaning that rebalancing across both sectors would result in higher bills for households and lower bills for businesses which is likely to be politically and economically undesirable.

- Business energy use is far more heterogeneous than households, with some very large users of gas. Changes to the balance of business energy costs should be part of a broader industrial strategy.

Downloads

-

Energy UK – Taking immediate action to make bills affordable this winter

Type: PDF (330 KB)